Before we go on to explore models of startup valuation, it is important to highlight that the value of an object represents its tangible worth, whereas its valuation entails a forecast of its perceived worth by individuals or a collective, albeit influenced by various factors. Similarly, many entrepreneurs or startup founders commonly perceive valuation as synonymous with their company’s worth, however, this notion is flawed. Valuation, instead, mirrors a set of projections regarding the company’s future performance, considering a number of very important factors that will be highlighted during the course of this piece. Kindly note that in the context of financing rounds, your startup’s valuation is ultimately reduced to what you and your investors agree that it is.

One of the most popular line you will hear in the startup world is that “valuing a startup is both an art and a science”. This statement holds in it real time truths. Figuring out a startup’s valuation is really like uncovering the treasure map to its potential riches! It’s the intricate journey of putting a price tag on those brilliant ideas and budding ventures.

Ordinarily, within each industry, a fundamental standard prevails which typically dictates the ultimate valuation of the companies that play within each industrial sector. For instance, a local retail enterprise is conventionally valued at a range of 1-2 times its annual earnings in addition to the assets or properties transferred alongside the transaction. Conversely, a technology startup demonstrating significant growth prospects is typically valued at a multiple of its anticipated future earnings, predicated upon its current growth trajectory.

Inflation of Valuation and Vanity Metrics

It is no news that a considerable number of startups exhibit valuations that are disproportionately inflated, stemming from unsubstantiated assertions and fictitious numerical representations. Investors: venture capitalists, angels and the likes are advised to be wary of the vanity metrics sold by the cutely put-together- graphic designs of blue collar wearing founders while navigating their way through fishing for a worthy venture.

https://giphy.com/gifs/startup-founder-venture-capital-NfxZS7rlbez0sCNkZo

It may interest investors to also consider that even the most viral product with heavy traction does not easily translate to real time profits. Let’s consider the case of a popular social media platform (name withheld for privacy reasons) which was reported to have recorded about 85 million users in 2015. At this time (in 2015), it was recorded to hold a valuation of $1billion. Just last year, the same platform was recorded to have onboarded approximately 360 million users while hanging on a $16 billion valuation. Regardless of these huge metrics, the social media platform is yet to record a profitable year, and what this means is that although the venture looks good on paper, its economics may yet not be the most investor friendly.

https://giphy.com/gifs/GrowthX-Club-zero-0-nil-r0q8JfQLzevKR24Anc

The lesson here is that vanity metrics, number of likes, downloads, users etc., although are important pointers, do not predict the profitability of a venture. This however, is not to discourage investors, but a factor to be considered. It is the smart investor that interrogates founders on how founders plan to be profitable with their ventures. It is also the smart founder that plans for how his or her venture will not just generate revenue, but also be profitable. The moral in the foregoing pretty much applies to other areas of life too; but let’s get back to this matter of startup valuation.

Careful of Founders Whose Business Model is Mere Fundraising

Another prevalent occurrence involves a subset of startups that have deviated from the pursuit of sustainable business models, genuine problem-solving, and value creation. Instead, they have adeptly optimized venture financing as an alternative business model, focusing primarily on fundraising endeavors and augmenting their valuation. Essentially, these unscrupulous founders’ real business is fund raising and not genuine problem solving.

In any event, the valuation of your startup holds significant relevance. Lower valuations necessitate a higher relinquishment of equity in the startup to procure investment. Conversely, higher valuations afford greater retention of equity within the company, thereby mitigating dilution and enhancing returns for stakeholders.

It’s been described that valuing a startup is both an art and a science. Determining the genuine valuation of a startup frequently entails gathering insights from comparable companies within the industry. Investors, spanning from venture capital firms and beyond typically assess competitors and industry peers to grasp how a company and its business model align with the prevailing landscape.

Quick one: As a prudent startup founder, you may also consult online databases like AngelList or Crunchbase to directly compare your valuation to similar businesses.

Common Startup Valuation Models

- The Berkus Method.

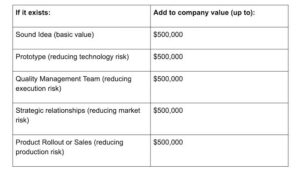

Developed by venture capitalist Dave Berkus to find valuations specifically for pre-revenue startups, the Berkus Method of Valuation is a technique designed for early-stage startups aiming to establish an initial valuation independent of the founder’s financial projections. This method assesses five key aspects of a startup and assigns a value ranging from zero to $500,000 for each area. The idea is to assign dollar amounts to five key success metrics found in early-stage startups. While Berkus Method of Valuation doesn’t consider additional market influences, its restricted scope proves beneficial for businesses seeking a straightforward assessment tool.

Here’s a concise overview:

Berkus Method Table

- Comparable Transactions Method.

This method is highly favored among startup valuation techniques due to its reliance on precedent. It addresses the query of, “What were the acquisition values of startups similar to mine?” The Comparative Transactions Method searches for past transactions that are similar or comparable, involving target companies for acquisition with analogous business models and comparable sizes as the startup in question.

Let’s use this Brex’s illustration:

For instance, imagine that Rapid, a fictional shipping startup, was acquired for $24 million. Its mobile app and website had 700,000 users. That’s roughly $34 per user. Your shipping startup has 120,000 users. That gives your business a valuation of about $4 million.

You can also seek out revenue multiples for comparable companies within your industry. For instance, in your market, it might be customary for Software as a Service (SaaS) companies to achieve revenue multiples ranging from 5 times to 7 times the net revenue of the preceding year.

- Cost-to-Duplicate Valuation Approach.

Just as the name implies, it entails determining the expense of replicating your startup elsewhere, excluding intangible assets such as brand reputation or goodwill.

You calculate by totaling the fair market value of your tangible assets, including research and development expenses, product prototype costs, patent expenditures, and similar items. Please take note that one significant limitation of this method is its inherent inability to fully encapsulate the company’s overall worth. It also overlooks crucial elements that hold particular relevance, such as intangible assets like brand reputation, patent rights, and customer engagement etc.

- Venture Capital Method.

Developed by Bill Sahlman, this is the commonly employed startup valuation model for VC firms. Below are two formulas you may employ to progress toward your startup’s valuation:

Anticipated Return on Investment (ROI) = Terminal Value ÷ Post-Money Valuation

Post-Money Valuation = Terminal Value ÷ Anticipated ROI. For a step by step explanation of this model, kindly refer to WallStreetPrep’s explicit explanation on the Venture Capital Method via the foregoing hyperlink. Also, you may dowload this VC Valuation form as prepared by the WallStreetPrep team.

- Book Value Method.

The book value method provides an asset-based valuation, akin to the cost-to-duplicate approach but with greater simplicity. Conventionally, a startup’s book value is calculated as the total assets minus liabilities. Essentially, the Book Value method equates the net worth of your startup with its valuation.

Bringing it all together.

While conducting a valuation of your business venture, it is advisable to test or use multiple valuation techniques to be able to come down to a fair valuation of your enterprise. Endeavour to evaluate both the tangible and intangibles of your startup. Tag a valuation on the strength of your team, size of the opportunity, product or service, competitive environment, marketing, sales channels, and partnerships, tangible assets, intangible assets, sound idea, quality team, workable prototype, forecasted revenue and profit, financials, last funding round, current revenue and company performance etc.

About the Author

Taiwo Lawal Esq. is a corporate and transactional lawyer. With about half a decade’s experience servicing startups (including on transactions regarding intellectual property rights), she is the founder of Unicorn Valley Law, doing what she loves the most- providing bespoke advisory from the “well of water” within her.

Taiwo is happy to read from you and provide bespoke solutions to your startup’s legal and commercial needs. Kindly write her via taiwo@unicornvalleylaw.com or schedule a call via calendly here: (get in touch).

{kind=link}